An increasingly sophisticated approach to running their businesses seems to be taking hold among solution providers in the channel.

According to an exclusive Solution Provider Business Practice survey of 273 solution providers conducted jointly by Ziff Davis Enterprise, publishers of Channel Insider and eWEEK, and the Crimson Consulting Group, which advises vendors on how to run their channel programs, over two-thirds of the 273 solution providers surveyed identified increasing business coming from new customers as one of their top priorities. Nearly as many said they are also focusing on increasing the percentage of revenue they derive from providing IT services.

In terms of providing those services, however, vendors seem to provide marginal assistance with about half of the solution providers surveyed saying that the support they get from big vendors is fair, good or worse. And when the results for the 47 percent of the solution providers in the survey that said they resell products are broken out separately, the opinion of the quality of support provided by vendors drops a little more.

In fact, it seems that most solution providers are focused on expanding their own services offerings rather than being dependent on vendors to provide those services.

For example, Alvaka Networks, in Irvine, Calif., is currently focused on creating a better structure for delivering higher quality of services.

“Our number one priority is to focus on our product development so we can create better packaging by providing more structure for our services,” said Alvaka Networks president Oli Thordarson.

Nevertheless, what solution providers seem to want most from the vendor community is improved customer support and more pre and post sales support for their people.

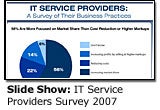

In general, solution providers appear to be optimistic about their business prospects. Half of the solution providers surveyed said they expect revenue growth to exceed 15 percent this year, while only 16 percent said they expected revenue growth to be unchanged or down.

But how solution providers intend to go about drumming up that new business is a little unclear. Only 42 percent of the solution providers surveyed said they planned to increase their investments in marketing even though more than half of them said they plan to increase their market share in 2007.

In addition, 60 percent of the solution providers surveyed said they have fewer than 150 customers and two-thirds of them confessed that they get 50 percent or more of their revenue from their top three largest customers. In fact, while solution providers as a whole rated themselves highly in terms of having technical acumen, they also agree that sales and marketing are their least-best skills, with those saying they resell products rating marketing as a strategic requirement lower than the rest of the solution provider community.

The need to increase the size of their customer base is one reason why the channel is experiencing a wave of mergers and acquisitions, as many solution providers have come to believe this is the fastest way to grow.

For example, Chips Computer Consulting of Lake Success, N.Y. last week acquired SBS Computer Service of Franklyn Square, N.Y. to increase its growth potential by acquiring a company that had a focus on smaller customers that Chips expects will grow into larger customers over the coming years.

“They’re essentially a smaller version of us with 60 clients,” said Chips Computer Consulting President Evan Leonard. “But they only have three employees.”

Overall, the survey results indicate that the channel is financially healthier than most people think, with 79 percent of those surveyed saying they were profitable in 2006. In order to stay that way, 60 percent of those surveyed said they intend to focus more in 2007 on providing higher value services, with application development and application integration topping the list of most strategic opportunities for accomplishing those goals. The next two areas of highest growth potential were systems management and managed services.

However, the 47 percent of the solution providers that actually resell products rated managed services as a top priority. And many solution providers such as Acropolis Technology Group in St. Louis are looking to expand beyond their existing remote managed service offerings to become providers of hosted applications and services that are run completely by the solution provider.

“We want to stay one step ahead of the herd by identifying what services will be picked off first in terms of becoming commodities,” said Acropolis President Tracy Butler. “We’re building out our hosting capability to provide more services more cost effectively as part of our effort to capture new customers.”

As part of that equation, the only places that companies that resell products differ from the rest of the solution providers is that they are slightly more concerned about profitability, given the razor-thin margins typically associated with selling products and they care a little more about vendors’ sales program and the reputation of their products. And finally, they are also more concerned with increasing market share compared with controlling costs than the rest of their solution provider brethren.

Overall, the study finds that the channel is in the middle of a major transformation.

“The channel landscape is changing rapidly,” said Allan Adler, a partner with Crimson Consulting. “Key factors that are driving solution provider behavior include the growth in services versus resale revenue, degree of specialization and new premium pricing strategies. The term VAR is now officially passé.”